AI Investment Frameworks with Francesca Warner, Ada Ventures

How do you quickly pitch (or for the angels among us, evaluate) a seed-stage company that is pre-revenue and perhaps even pre-product?

Francesca (Check) Warner MBE is the co-founder of Ada Ventures, Europe’s first VC fund focused on diverse founders building breakthrough ideas for the hardest problems we face. A columnist at Forbes covering venture capital and entrepreneurship, Check shares her insights on developing robust investment frameworks for seed stage AI startups…

We first published our model for evaluating companies (A Seed Investing Framework) six years ago, and still apply a version of this framework today. We believe you need an evolved framework for Investing in AI-first companies at pre-seed and seed. I hope that it is a useful prompt to founders already working and those considering building in this space. This framework is meant to spark a discussion and I would love input here.

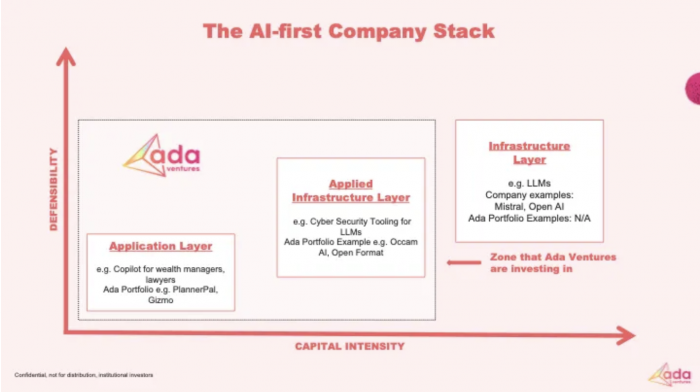

Very simply we see there being three ‘layers’ to the AI-first Company (software) stack. For each of these ‘layers’ there are different considerations that an investor has to weigh up — so we’ve mapped these on a graph with the X-axis being capital intensity and the y-axis being defensibility. Our hypothesis is that Infrastructure Layer companies are the most capital intensive but also more defensible, application layer companies are the least defensible but also the least capital intensive. For the Applied Infrastructure Layer, the companies are less capital intensive than building a foundational model, but still require hiring top developer talent and large engineering teams. They likely have a longer go to market (usually bottom up via developers) and therefore have a longer time to value. They get more deeply embedded into the stack and therefore switching costs are higher and are therefore more defensible.

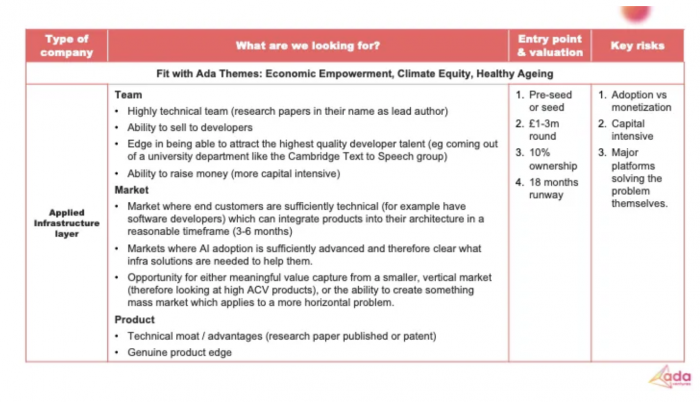

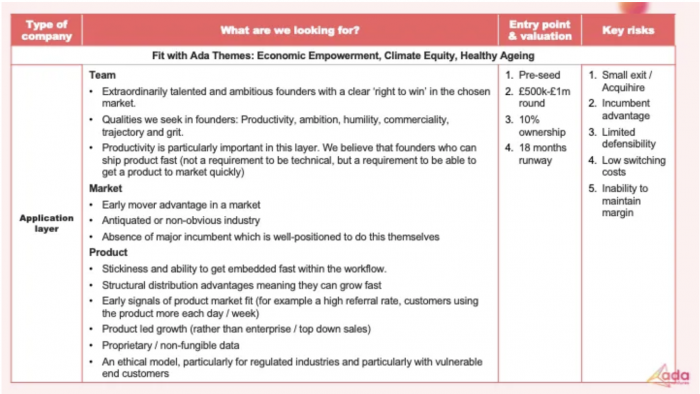

We think that there are very valuable companies to be built at both the Applied Infrastructure and the Application Layers — but there are different considerations for founders and investors. Our Framework for what we’re looking for in Applied Infrastructure and Application Layer companies is below, alongside our ideal entry price and the key risks we are looking at at each layer.

Infrastructure Layer — Eg. LLMs. Company examples: Mistral, Open AI, Ada Portfolio eg: N/A

At Ada Ventures, we are generally not investing in Infrastructure Layer companies. We don’t have deep enough pockets to fund the compute costs for Large Language Models that require massive GPU clusters, especially with sovereign funds and trillion dollar tech companies funding them. There was initially a view that these companies would be defensible due to their data advantages, but more recently we’ve seen similar performance from models trained on smaller datasets and also customers willingness to switch from one model to another. So whether these truly are more defensible than other types of AI-first companies is unclear. However — these are still very capital intensive to build and that does create a moat of sorts.

Applied Infrastructure Layer (Eg. Cyber Tooling for LLMs, model supervision, fine tuning). Eg LangChain, Ada Portfolio eg. Occam AI (Occam AI sells an ‘embedded agents’ API that are designed to give existing enterprise software intelligent automation capabilities).

These companies are building core technology that adapts some aspect of the Infrastructure Layer to make it more usable or address a more specific use case. For example, a company building cyber security tooling which sits on top of an LLM which makes it more secure, in order that it can be usable by financial services companies. Applied Infrastructure companies typically go to market via developers and help developers ship more products more quickly and ensure that those products are performing correctly. The depth of focus on a technical breakthrough means that these companies tend to be more capital intensive since they tend to need bigger engineering teams. However, the prize could be bigger if they are successful.

Application Layer (Eg. Copilot for lawyers eg. Harvey). Ada Portfolio eg. Gizmo, PlannerPal.

Finally, the least capital intensive companies are the Application Layer companies. These can typically be built with a small team and companies can start to achieve revenue traction as companies and individuals are experimenting with new tools. Application Layer companies are those that are using GenAI, often building on top of closed or open-source models and building applications to solve end user problems, whether B2B or B2C users. This layer could be an attractive place to invest. We are particularly intrigued by vertical companies building customised solutions to their industry (for example PlannerPal in Wealth Management) and marketplaces (B2B or B2C) like Gizmo in education. With this layer, founders must be mindful of building a moat and increasing defensibility to build a true long term competitive advantage. Compelling ways that we have seen founders build defensibility in this layer are:

- Encouraging user generated content — by incentivising users to add their own proprietary data to the product, the product is personalised and enriched, making it stickier.

- Tackling a regulated industry which has specific domain specific requirements, meaning that generic LLMs find it harder to tackle.

- Being an early mover in the market and getting embedded within the workflow and used daily by customers.

- Building for a specific vertical so that the tools, language and approach can be tailored to suit this vertical.

- Network effects in the business model

More on what Ada Ventures invests in and Impact risks for AI-first companies here